PHP Market Update

22 Jul 2026 • 00:33 GMT

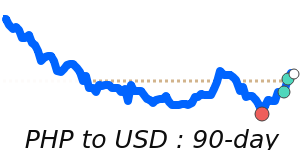

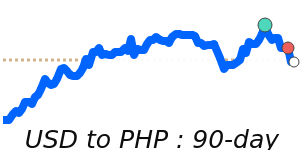

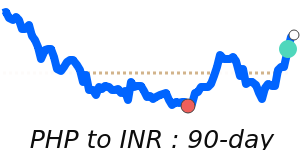

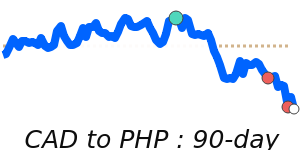

The Philippine peso continues to face pressure amid global risk trends and US dollar strength. Recently, PHP has dipped to near 30-day lows around 0.016185, slightly below its 3-month average of 0.016312. This suggests a small but potentially sustained weakening against the dollar, influenced by ongoing geopolitical uncertainties and a relatively stronger US dollar driven by safe-haven flows and expectations of Federal Reserve rate hikes.

While the peso has remained within a stable trading range, the overall outlook remains cautious. The US dollar has been supported by tensions in the Middle East, boosting safe-haven demand and oil prices. Meanwhile, the peso’s decline past the key level of ₱60 per US dollar in March reflects global uncertainties and domestic economic factors.

If US rate hikes continue or geopolitical tensions escalate, the PHP may experience further downward pressure. Conversely, positive domestic developments or easing geopolitical risks could support a stabilization or modest recovery for the peso. For now, markets remain watchful of US dollar movements and regional geopolitical cues that could influence the PHP’s outlook through the remainder of the year.

📊 Quick forecast view

🔴 Mild downside

0.0160 – 0.0170

🏦 Central bank policy divergence

🟢 Uptrend