PLN Market Update

27 Jun 2026 • 01:14 GMT

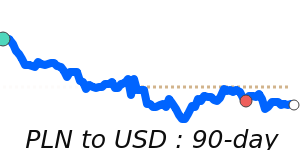

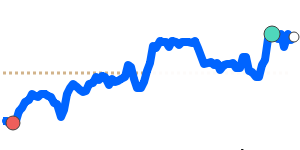

The Polish zloty (PLN) remains relatively stable against major currencies, despite the recent strength of the US dollar. Currently, the PLN/USD exchange rate stands at around 0.2656, which is about 2.9% below its 3-month average of 0.2734. This indicates some softness versus the dollar but within a stable trading range, as the pair has traded between roughly 0.2651 and 0.2787 over recent months.

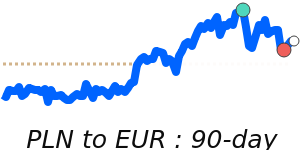

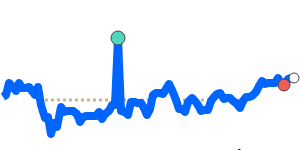

The USD's rally, driven by rising expectations of a September interest rate hike from the Federal Reserve and increased risk aversion, continues to put pressure on emerging-market currencies like the PLN. Meanwhile, the euro has seen the PLN/EUR near its 60-day lows, trading just 0.9% below its recent average, reflecting cautious sentiment.

Overall, the PLN's performance remains supported by Poland's steady economic growth and improved inflation outlook, though the USD's strength remains a key factor. With the US dollar remaining strong, traders should watch for any shifts in global risk sentiment or central bank signals that could influence the zloty’s short-term direction.

📊 Quick forecast view

🔴 Mild downside

0.2610 – 0.2660

🌍 Global risk sentiment

🟢 Uptrend